Open to work

Designing a New Way to Pay: From Rapid Launch to Sustainable Growth.

Using rapid discovery to launch an annual payment model, expanding our market reach, and supporting customers through an economic crisis.

Role

Product designer

Results

New “pay in full” variant covered 60-70% of new business and opened a new revenue channel.

Our overall price comparison site “click to purchase” rate improved, taking us closer to the industry baseline.

Cancellations with the reason “didn’t understand the policy” went down, saving the business ~£150 per member.

Context.

By Miles is the UK’s first pay-by-mile car insurer, designed to provide fairer pricing for lower-mileage drivers. Their insurance model is split into two distinct parts: a fixed annual premium to cover the car while it is parked, and a variable per-mile rate for the distance actually driven.

The problem.

Despite strong performance on Price Comparison Websites, we faced a significant conversion hurdle: high-intent visitors were dropping off at the final stage of our quote journey. We were successfully attracting users who wanted the fairness of pay-by-mile, but we were failing to convert them into active policyholders.

At the start of the project, we knew the what (the drop-off), but we didn't yet understand the why.

The mini design sprint.

I co-led a three-day intensive design sprint with Engineering, Customer Support, and Product to uncover the root cause of this friction.

Day 1: Building a hypothesis

By exploring the problem and facilitating a Jobs To Be Done workshop, we converged four primary hypotheses. The most popular one assumed that payment schedule was the problem. While users appeared to be buying an annual policy, they discovered late in the flow that they would still be billed monthly for their miles.

Day 2: Testing assumptions

I conducted moderated customer research sessions that confirmed this "expectation gap". Users looking for a yearly policy expected a single, "set and forget" transaction. The discovery of an ongoing monthly commitment felt like a "hidden" administrative burden – consistent with month 1 “bill shock” cancellations.

Day 3: Validating a solution

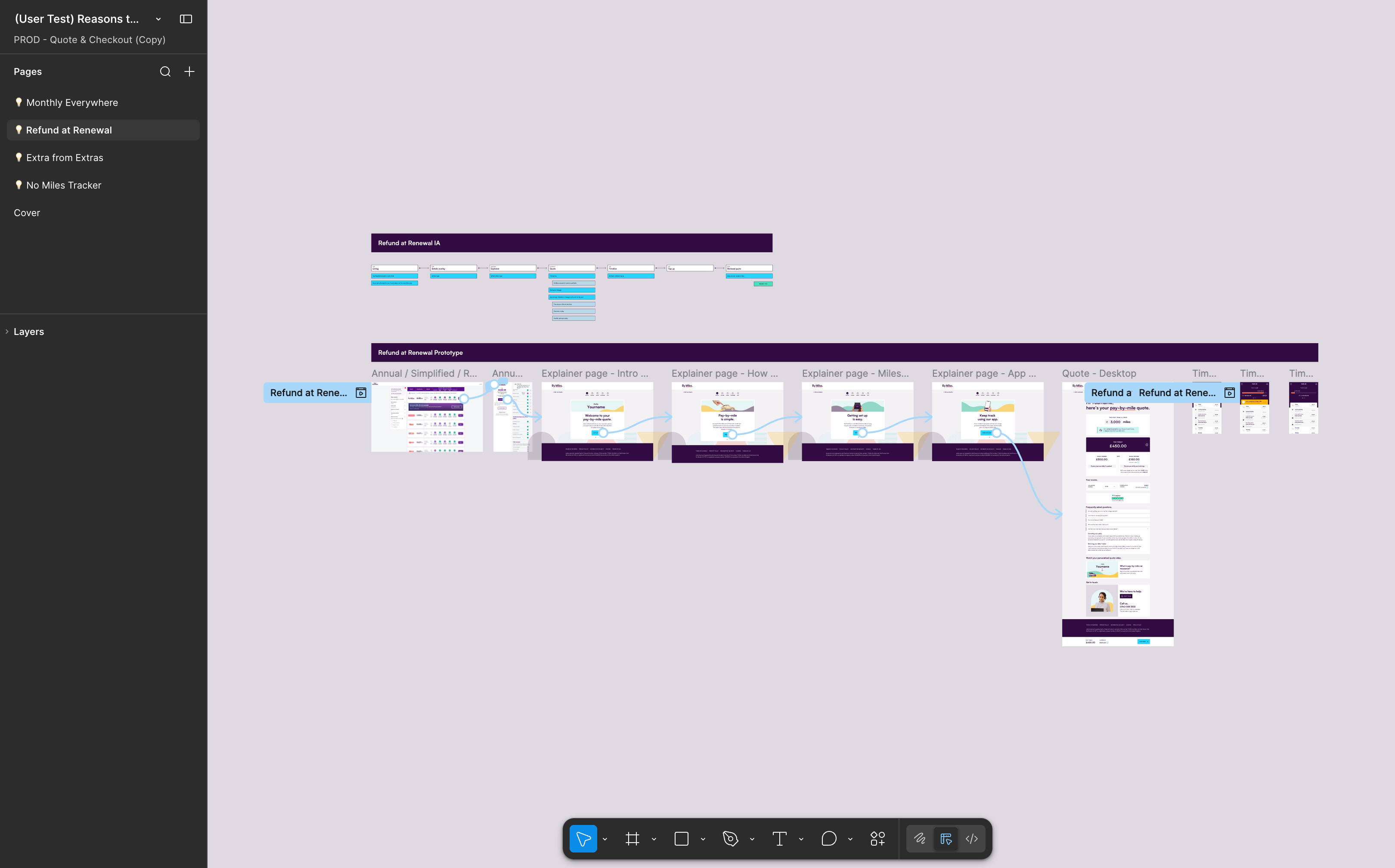

I developed a rapid prototype of a "Pay in Full" model – an upfront annual premium including a prepaid balance of miles that are refunded at the end of the year, removing monthly billing (unless prepaid miles are used up).

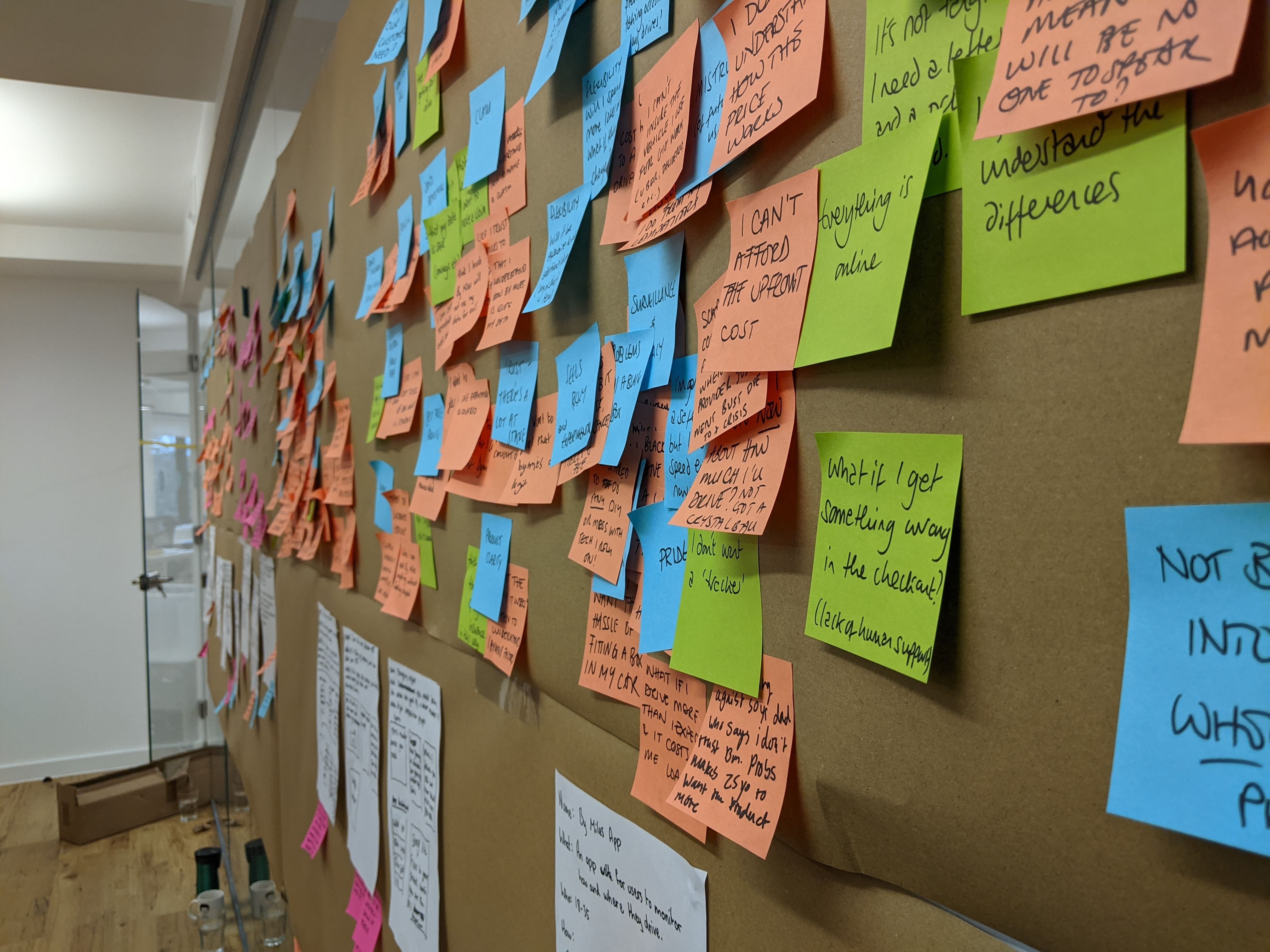

Some of the output from a divergent thinking exercise to explore team assumptions around why customers were dropping off, based on emotional, functional and social jobs.

A rough, simplified customer journey prototyped I used in an unmoderated user test to gauge how customers felt about the “refund at renewal” proposition.

Launching “Refund at renewal”

A major challenge was the app’s technical architecture, which was read-only at the time. Building a full self-service tool for users to top up their miles balance would have required a massive engineering project.

I identified through quote data that the pay yearly cohort significantly over-estimates their annual mileage. Leveraging this insight, I proposed a launch strategy focused on customers who over-estimate their mileage – a group I identified by querying our existing quote data. By launching a Minimum Loveable Product where infrequent top-ups were handled manually by our support team, we were able to go to market months earlier and validate commercial demand.

Making a strategic tradeoff

I identified through quote data that the pay yearly cohort significantly over-estimates their annual mileage. Leveraging this insight, I proposed a launch strategy focused on customers who over-estimate their mileage – a group I identified by querying our existing quote data. By launching a Minimum Loveable Product where infrequent top-ups were handled manually by our support team, we were able to go to market months earlier and validate commercial demand.

The impact

We launched the annual payment option as a pilot on a single Price Comparison Website.

- The new model led to a marked increase in conversions for pay yearly customers coming from price comparison sites.

- The variant was an overnight success, accounting for 60-70% of all new business within a few months.

© 2025 - 2026 Daniel van der Spuy

Get in touch:

hi@danvan.design

Connect with me on

Open to work

Designing a New Way to Pay: From Rapid Launch to Sustainable Growth.

Using rapid discovery to launch an annual payment model, expanding our market reach, and supporting customers through an economic crisis.

Using rapid discovery to launch an annual payment model, expanding our market reach, and supporting customers through an economic crisis.

Role

Product designer

Results

New “pay in full” variant covered 60-70% of new business and opened a new revenue channel.

Our overall price comparison site “click to purchase” rate improved, taking us closer to the industry baseline.

Cancellations with the reason “didn’t understand the policy” went down, saving the business ~£150 per member.

Context.

By Miles is the UK’s first pay-by-mile car insurer, designed to provide fairer pricing for lower-mileage drivers. Their insurance model is split into two distinct parts: a fixed annual premium to cover the car while it is parked, and a variable per-mile rate for the distance actually driven.

The problem.

Despite strong performance on Price Comparison Websites, we faced a significant conversion hurdle: high-intent visitors were dropping off at the final stage of our quote journey. We were successfully attracting users who wanted the fairness of pay-by-mile, but we were failing to convert them into active policyholders.

At the start of the project, we knew the what (the drop-off), but we didn't yet understand the why.

The mini design sprint.

I co-led a three-day intensive design sprint with Engineering, Customer Support, and Product to uncover the root cause of this friction.

Day 1: Building a hypothesis

By exploring the problem and facilitating a Jobs To Be Done workshop, we converged four primary hypotheses. The most popular one assumed that payment schedule was the problem. While users appeared to be buying an annual policy, they discovered late in the flow that they would still be billed monthly for their miles.

Day 2: Testing assumptions

I conducted moderated customer research sessions that confirmed this "expectation gap". Users looking for a yearly policy expected a single, "set and forget" transaction. The discovery of an ongoing monthly commitment felt like a "hidden" administrative burden – consistent with month 1 “bill shock” cancellations.

Day 3: Validating a solution

I developed a rapid prototype of a "Pay in Full" model – an upfront annual premium including a prepaid balance of miles that are refunded at the end of the year, removing monthly billing (unless prepaid miles are used up).

Some of the output from a divergent thinking exercise to explore team assumptions around why customers were dropping off, based on emotional, functional and social jobs.

A rough, simplified customer journey prototyped I used in an unmoderated user test to gauge how customers felt about the “refund at renewal” proposition.

Launching “Refund at renewal”

A major challenge was the app’s technical architecture, which was read-only at the time. Building a full self-service tool for users to top up their miles balance would have required a massive engineering project.

I identified through quote data that the pay yearly cohort significantly over-estimates their annual mileage. Leveraging this insight, I proposed a launch strategy focused on customers who over-estimate their mileage – a group I identified by querying our existing quote data. By launching a Minimum Loveable Product where infrequent top-ups were handled manually by our support team, we were able to go to market months earlier and validate commercial demand.

Making a strategic tradeoff

I identified through quote data that the pay yearly cohort significantly over-estimates their annual mileage. Leveraging this insight, I proposed a launch strategy focused on customers who over-estimate their mileage – a group I identified by querying our existing quote data. By launching a Minimum Loveable Product where infrequent top-ups were handled manually by our support team, we were able to go to market months earlier and validate commercial demand.

The impact

We launched the annual payment option as a pilot on a single Price Comparison Website.

- The new model led to a marked increase in conversions for pay yearly customers coming from price comparison sites.

- The variant was an overnight success, accounting for 60-70% of all new business within a few months.

© 2025 - 2026 Daniel van der Spuy

Get in touch:

hi@danvan.design

Connect with me on

Open to work

Role

Product designer

Results

New “pay in full” variant covered 60-70% of new business and opened a new revenue channel.

Our overall price comparison site “click to purchase” rate improved, taking us closer to the industry baseline.

Cancellations with the reason “didn’t understand the policy” went down, saving the business ~£150 per member.

Designing a New Way to Pay: From Rapid Launch to Sustainable Growth.

Using rapid discovery to launch an annual payment model, expanding our market reach, and supporting customers through an economic crisis.

Context.

By Miles is the UK’s first pay-by-mile car insurer, designed to provide fairer pricing for lower-mileage drivers. Their insurance model is split into two distinct parts: a fixed annual premium to cover the car while it is parked, and a variable per-mile rate for the distance actually driven.

The problem.

Despite strong performance on Price Comparison Websites, we faced a significant conversion hurdle: high-intent visitors were dropping off at the final stage of our quote journey. We were successfully attracting users who wanted the fairness of pay-by-mile, but we were failing to convert them into active policyholders.

At the start of the project, we knew the what (the drop-off), but we didn't yet understand the why.

The mini design sprint.

I co-led a three-day intensive design sprint with Engineering, Customer Support, and Product to uncover the root cause of this friction.

Day 1: Building a hypothesis

By exploring the problem and facilitating a Jobs To Be Done workshop, we converged four primary hypotheses. The most popular one assumed that payment schedule was the problem. While users appeared to be buying an annual policy, they discovered late in the flow that they would still be billed monthly for their miles.

Day 2: Testing assumptions

I conducted moderated customer research sessions that confirmed this "expectation gap". Users looking for a yearly policy expected a single, "set and forget" transaction. The discovery of an ongoing monthly commitment felt like a "hidden" administrative burden – consistent with month 1 “bill shock” cancellations.

Day 3: Validating a solution

I developed a rapid prototype of a "Pay in Full" model – an upfront annual premium including a prepaid balance of miles that are refunded at the end of the year, removing monthly billing (unless prepaid miles are used up).

Some of the output from a divergent thinking exercise to explore team assumptions around why customers were dropping off, based on emotional, functional and social jobs.

A rough, simplified customer journey prototyped I used in an unmoderated user test to gauge how customers felt about the “refund at renewal” proposition.

Launching “Refund at renewal”

A major challenge was the app’s technical architecture, which was read-only at the time. Building a full self-service tool for users to top up their miles balance would have required a massive engineering project.

Making a strategic tradeoff

I identified through quote data that the pay yearly cohort significantly over-estimates their annual mileage. Leveraging this insight, I proposed a launch strategy focused on customers who over-estimate their mileage – a group I identified by querying our existing quote data. By launching a Minimum Loveable Product where infrequent top-ups were handled manually by our support team, we were able to go to market months earlier and validate commercial demand.

The impact

We launched the annual payment option as a pilot on a single Price Comparison Website.

- The new model led to a marked increase in conversions for pay yearly customers coming from price comparison sites.

- The variant was an overnight success, accounting for 60-70% of all new business within a few months.

© 2025 - 2026 Daniel van der Spuy

Get in touch:

hi@danvan.design

Connect with me on